Which of the following will have the effect of increasing the duration of a bond, all else remaining equal:

I. Increase in bond coupon

II. Increase in bond yield

III. Decrease in coupon frequency

IV. Increase in bond maturity

An investor enters into a 4 year interest rate swap with a bank, agreeing to pay a fixed rate of 4% on a notional of $100m in return for receiving LIBOR. What is the value of the swap to the investor two years hence, immediately after the net interest payments are exchanged? Assume the 2 year swap rate is 5%, and the yield curve is also flat at 5%

A US treasury bill with 90 days to maturity and a face value of $100 is priced at $98. What is the annual bond-equivalent yield on this treasury bill?

Which of the following statements are true:

I. The convexity of a zero coupon bond maturing in 10 years is more than that of a 4% coupon bond with a modified duration of 10 years

II. The convexity of a bond increases in a linear fashion as its duration is increased

III. Convexity is always positive for long bond positions

IV. The convexity of a zero coupon bond maturing in 10 years is less than that of a 4% coupon bond maturing in 10 years

A large utility wishes to issue a fixed rate bond to finance its plant and equipment purchases. However, it finds it difficult to find investors to do so. But there is investor interest in a floating rate note of the same maturity. Because its revenues and net income tend to vary only predictably year to year, the utility desires a fixed rate liability. Which of the following will allow the utility to achieve its objectives?

How will the Macaulay duration of a 10 year coupon bearing bond change if 10 year zero rates stay the same but the yield curve changes from being flat to upward sloping?

Which of the following statements is true in relation to the capital markets line (CML):

I. The CML is a transformation line that is tangential to the efficient frontier

II. The CML allows an investor to obtain the highest return for a given level of risk chosen according to the investor's risk attitude

III. The CML is the line passing through the point on the efficient frontier with the highest Sharpe ratio, and a y-intercept equal to the risk free rate

IV. The Sharpe ratio for the points on the CML increase in a linear fashion

Which of the following statements are true?

I. Macaulay duration of a coupon bearing bond is unaffected by changes in the curvature of the yield curve.

II. The numerical value for modified duration will be different for bonds with identical nominal coupons and maturity but different compounding frequencies.

III. When rates are expressed as continuously compounded, modified duration and Macaulay duration are the same.

IV. Convexity is higher for a bond with a lower coupon when compared to a similar bond with a higher coupon.

By market convention, which of the following currencies are not quoted in terms of 'direct quotes' versus the USD?

An investor enters into a 4 year interest rate swap with a bank, agreeing to pay a fixed rate of 4% on a notional of $100m in return for receiving LIBOR. What is the value of the swap to the investor two years hence, immediately after the net interest payments are exchanged? Assume the current zero coupon bond yields for 1, 2 and 3 years are 5%, 6% and 7% respectively. Also assume that the yield curve stays the same after two years (ie, at the end of year two, the rates for the following three years are 5%, 6%, and 7% respectively).

Which of the following statements are true:

I. The swap rate, also called the swap spread, is initially calculated so that the value of the swap at inception is zero.

II. The value of a swap at initiation is different from zero and is equal to the difference between the NPV of the cash flows of the two legs of the swap

III. OTC swaps are standardized and limited to a defined set of standard contracts

IV. Interest rate and commodity swaps are the types of swaps that are most traded

A company has a long term loan from a bank at a fixed rate of interest. It expects interest rates to go down. Which of the following instruments can the company use to convert its fixed rate liability to a floating rate liability?

For a forward contract on a commodity, an increase in carrying costs (all other factors remaining constant) has the effect of:

Which of the following statements is true:

I. A high market beta implies a high degree of correlation with the market

II. Correlation coefficient and covariance between assets have the same sign

III. A correlation of zero indicates the absence of a linear relationship between the two assets

IV. Unless assets are perfectly correlated, diversification always reduces portfolio risk.

It is October. A grower of crops is concerned that January temperatures might be too low and destroy his crop. A heating-degree-days futures contract (HDD futures contract) is available for his city. What would be the best course of action for the grower?

A stock has a spot price of $102. It is expected that it will pay a dividend of $2.20 per share in 6 months. What is the price of the stock 9 months forward? Assume zero coupon interest rates for 6 months to be 6%, for 9 months to be 7%, and 12 months to be 8% - all continuously compounded.

Continuously compounded returns for an asset that increases in price from S1 to S2 over time period t (assuming no dividends or other distributions) are given by:

Which of the following indicate a long position on the TED (treasury-Eurodollar) spread?

What is the fair price for a bond paying annual coupons at 5% and maturing in 5 years. Assume par value of $100 and the yield curve is flat at 6%.

Calculate the basis point value, or PV01, of a bond with a modified duration of 5 and a price of $102.

A borrower who fears a rise in interest rates and wishes to hedge against that risk should:

For a portfolio of equally weighted uncorrelated assets, which of the following is FALSE:

If a firm is financed equally by debt and equity, and the cost of debt is 10% per annum and the cost of equity is 14%, what is the weighted average cost of capital for the firm if taxes are 25%?

An investor holds $1m in a 10 year bond that has a basis point value (or PV01) of 5 cents. She seeks to hedge it using a 30 year bond that has a BPV of 8 cents. How much of the 30 year bond should she buy or sell to hedge against parallel shifts in the yield curve?

An investor holds $1m in face each of two bonds. Bond 1 has a price of 90 and a duration of 5 years. Bond 2 has a price of 110 and a duration of 10 years. What is the combined duration of the portfolio in years?

Which of the following is true about the early exercise of an American call option:

Which of the following statements is true:

I. On-the-run bonds are priced higher than off-the-run bonds from the same issuer even if they have the same duration.

II. The difference in pricing of on-the-run and off-the-run bonds reflects the differences in their liquidity

III. Strips carry a coupon generally equal to that of similar on-the-run bonds

IV. A low bid-ask spread indicates lower liquidity

An investor has a portfolio with a value of $1,000,000 and a beta of 2.5. He believes the portfolio carries more market risk than he desires and wishes to reduce the beta to 1. How many futures contracts should be buy or sell to reduce the beta if the futures contracts have a beta of 1.2 and the notional value of each contract is $240,000?

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

The profit potential from the conversion of convertible bonds into stock is limited by

Which of the following statements are true in respect of a fixed income portfolio:

I. A hedge based on portfolio duration is valid only for small changes in interest rates and needs periodic readjusting

II. A duration based portfolio hedge can be improved by making a convexity adjustment

III. A long position in bonds benefits from the resulting negative convexity

IV. A duration based hedge makes the implicit assumption that only parallel shifts in the yield curve are possible

A stock that pays no dividends is trading at $100 spot or $104 as a three month forward. The interest rate you can borrow at is 6% per annum. US treasury yields are 4% per annum. What should you do to profit in the situation?

PRM Certification | 8006 Questions Answers | 8006 Test Prep | Exam I: Finance Theory Financial Instruments Financial Markets - 2015 Edition Questions PDF | 8006 Online Exam | 8006 Practice Test | 8006 PDF | 8006 Test Questions | 8006 Study Material | 8006 Exam Preparation | 8006 Valid Dumps | 8006 Real Questions | PRM Certification 8006 Exam Questions

TESTED 26 Apr 2025

103.04.e2

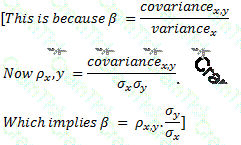

103.04.e2 103.04.e2, where x is the market portfolio and y is the asset under consideration.

103.04.e2, where x is the market portfolio and y is the asset under consideration. 103.04.e

103.04.e